There are many ways to increase your credit score. There are many options available to you, including paying off your debt on time or disputing inaccurate information on your credit report. You can apply for a new credit line, address credit reporting inaccuracies, or get a new credit card.

Paying down debt on time

One of the most important things that you can do to raise your credit score is to pay down your debt on time. Your score is calculated from several factors. Having a low balance on credit cards will boost your score, and will help you qualify for lower interest rates. Try to reduce your debt as quickly as possible if you don't have the money to pay it off.

Your goal should be to keep your debt levels below 20% of your credit limit. This will lower credit utilization ratio. It is the ratio of how much you owe to the credit available. Your credit score will rise if you keep your balances below 20 percent. You can also set up alerts for reminders and help you remember when your payments are due. You could also contact credit card companies and ask them for a greater credit limit. It shouldn't take much time.

Applying to another credit card

There are several things you can do quickly to increase your credit score. First, you should avoid applying for cards that have annual fees. To make the annual fee worthwhile, you may need to take advantage of the rewards programs offered by these cards. When you apply for new credit cards, make sure to not increase your credit card spending. This will decrease your credit utilization rate and improve your score.

Third, limit your new credit card use to less than 30% of your available credit. This will lower your credit utilization ratio to less that 20%. Your credit score can be significantly improved by using only a portion of your available credit. Not using all your available credit is a good idea. It can make it appear that you are a risky borrower.

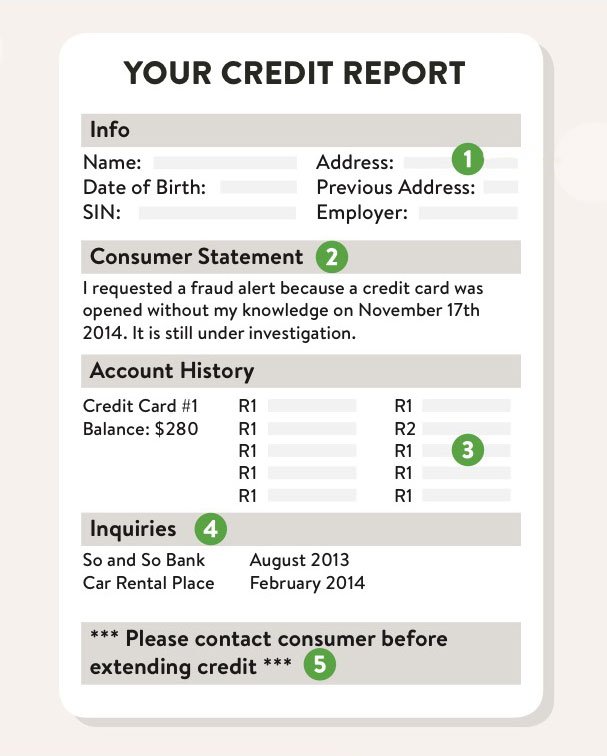

Resolve inaccuracies in your credit report

You can dispute inaccurate credit information by filing a dispute with your credit bureau. You can dispute the information online or by contacting your account provider. Include copies of supporting documentation. Credit scores can be affected by how quickly a dispute is resolved.

Follow up with the credit bureau if your dispute doesn't result in a reasonable time. They should send you a written response and an updated copy of your credit report. The dispute does not count against your free annual credit report, but it can appear on future reports. A copy of the dispute statement may require you to pay a fee. The credit bureau has provided a sample dispute letter to help you ensure the correct response. Make sure you send the dispute letters by certified mail.

Taking out a non-revolving credit line

Credit scores show how attractive a borrower can be to lenders. Although there are many different formulas used, most lenders look at five factors when calculating credit scores. One of these is the ratio of a borrower's debt to their credit limit. Your credit score will improve if you lower your credit utilization rate. You can also increase your credit limit by paying off your outstanding balances.

Inactivity on credit card accounts can affect credit scores. FICO likes to see recent activity on revolving accounts. Although not all cards must have a balance on them, it can affect your score if there isn't enough activity.

Applying for a secured card

Bad credit can make it difficult to get a secured creditcard. Secured cards require a deposit and report a good payment history to the credit bureaus. The card should only be used responsibly. You should keep your balance below 30% of the credit limit. There are many kinds of secured credit options available.

Secured credit cards require that you deposit equal to the credit limit you will receive. Save money for this deposit. Once approved, you should choose a card offering low deposits and reasonable credit lines. You will avoid interest accruing if you pay off your balance each month in full.