Even if your child is still young, it's not too late to build credit. Children typically don't have many lines but can start with one. Teens can start credit building right away. Creditors will ask how often the young person requests additional credit. If the young person makes many requests, it could be a sign that they are a higher-risk borrower.

Piggybacking

Piggybacking is an excellent way to increase your credit score. However, it will only take you so far. Your best chance to improve your credit score is to borrow responsibly and practice good credit behavior. You can have your parent sign for you. Be responsible when opening new credit accounts.

Piggybacking an account with an established cardholder can be a great way to build credit and improve your credit score if you're young. However, this is not a guarantee so you need to weigh the rewards and risks.

Authorized usership

By adding your child as an approved user to your credit account, you can help your child build credit. But, it is important that your teen adheres to the rules when using the card responsibly. Bad credit can damage your credit rating, as well as that of your teen. To avoid this situation, consider a few ways to protect your teen's credit.

Many parents believe that starting to build credit at 16 is the best time. It is also when many young adults first start driving and work. Credit-building at this young age is also an important part of learning how to handle money, save money, and plan for college.

Co-signing

A co-signing agreement for a credit line is an option to help your child get started with credit building. It is not uncommon to co-sign for another account, but it comes with some risks. If the borrower does not pay, the cosigner will become responsible for the payments. Late payments could affect the borrower’s credit score. This is a great way for your child to start building credit.

While a co-signing loan puts a parent at financial risk, it can also teach your child about money management and the importance of making regular payments. Your child will probably have a higher credit score than they would otherwise. Your child's financial future will be protected if you teach them as a parent.

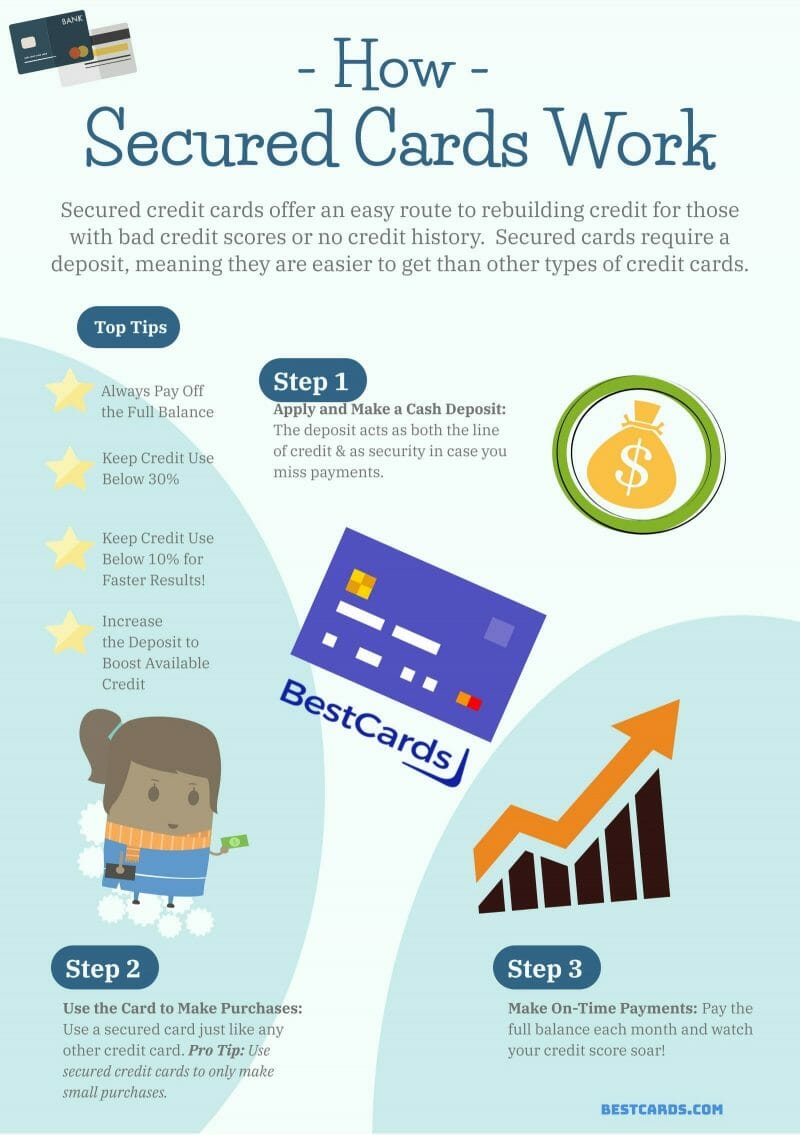

Secured credit cards

Secured credit cards can be a great way for you to build your credit. This type of card requires an initial deposit that acts as your credit limit. These cards can not be used to exceed your credit limit, unlike unsecured credit card. It will also report the credit bureaus about your payment history.

Secured credit cards can help you build credit even if you're a teenager or pre-teen. These cards are a good option for anyone who hasn't established a stable income. They work exactly like credit cards, but they require a security investment from the cardholder. In the event of default by the cardholder, the security deposit acts as collateral. In most cases, the card's credit limit is determined by the security deposit.

Add a child in as an authorized user

To help your child begin building credit, it is a smart idea to add a child as an authorized credit card user. This will allow you to monitor your child's spending habits. Before your child can make any charges it is important to clearly communicate your expectations. Keep in mind that major charges may affect your credit scores and credit history if your child is convicted.

Once you have authorized your child, the issuer can send your child their child's credit card. It will include their name. It's important to do this because they will link their account to yours. Unpaid bills can damage your credit. Your child can be added as an authorized user to help them build a credit history and teach them responsibility. This will help your child get a credit card faster when they turn 18.